Innovation in the solar photovoltaic industry

An innovation-focused roadmap for a sustainable global photovoltaic industry

Cheng Zheng and Daniel M. Kammen*

Energy Policy 2014, DOI: 10.1016/j.enpol.2013.12.006

In this paper, we collected a comprehensive dataset of the PV industry during 2000-2012, and framed the data in perspectives. By examining the current industry status, we developed a set of policy recommendations for a sustainable global PV industry going forward.

We started this policy analysis, as we are very concerned that a troubling PV industry could significantly diminish the outlook of mitigating climate change on the global scale.

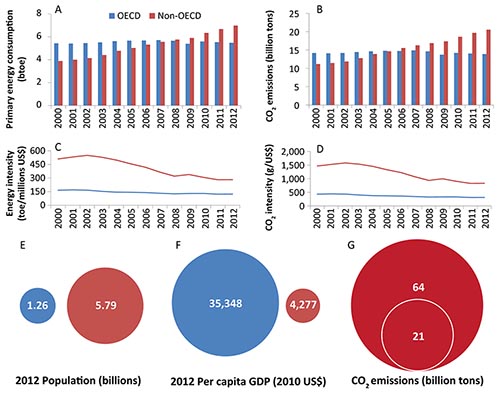

Fig. 1. Implications of global economic growth on CO2 emission targets. (Please refer to the paper for details.)

Fig. 1 shows the energy consumption, CO2 emissions, energy intensity, CO2 intensity, population, and economic prosperity since the beginning of the 21st century by two groups of nations: the rich OECD nations and the non-OECD nations. Although the energy consumption and CO2 emissions from the OECD nations has stabilized, the energy consumption from the non-OECD nations has increased by 79% between 2000 and 2012, and the associated CO2 emissions have increased by 84%. Due to a much larger population from the non-OECD nations, the overall energy consumption and CO2 emissions globally have increased by 34% and 36%, respectively. The implication of this simple math is very clear: If our goal is for everyone on this planet to have similar economic prosperity as the people living in the OECD nations, in a business-as-usual scenario, the energy-related carbon emissions from the non-OECD nations would almost triple from its current level. The net effect will overwhelm any climate change mitigation efforts from the rich OECD nations. Therefore, we need to tackle this grand energy challenge of the 21st century by both using energy more efficiently and developing more affordable low-carbon energy sources.

When we frame the 2000-2012 data of the global PV industry in different perspectives, we start to see what went wrong in the PV industry globally. From the national perspective, the PV industry has a truly globalized value chain. Germany is the top market for PV deployment, and China is the top manufacturer of PV modules. While the US and Japan are still the top two innovators in PV technology, despite their diminishing share in manufacturing and market size over the decade.

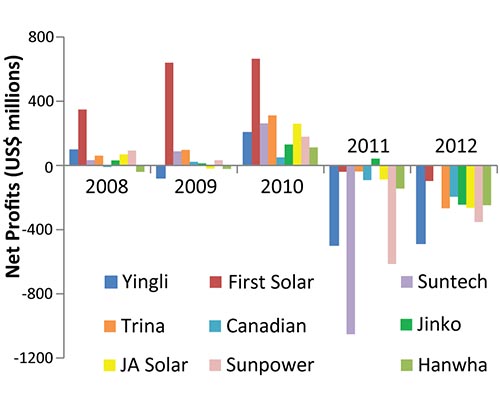

Fig. 2. Net profits (losses)of 9 major US-listed PV manufacturers during 2008–2012. (Please refer to the paper for details.)

From the manufacturers' perspectives, the PV industry is going through serious financial difficulties at the moment, with all of these top US-listed PV manufacturers losing money in 2012 (in Fig. 2).

From the smaller PV technology startups' perspectives, now is a difficult time to scale up innovative technologies, as we saw many of these companies going bankrupt or being acquired in the recent few years.

From the venture capital's perspectives, these poor financial scorecards of the PV industry were largely responsible for a dramatic shrinking in venture capital support for solar technologies between 2008 and 2012.

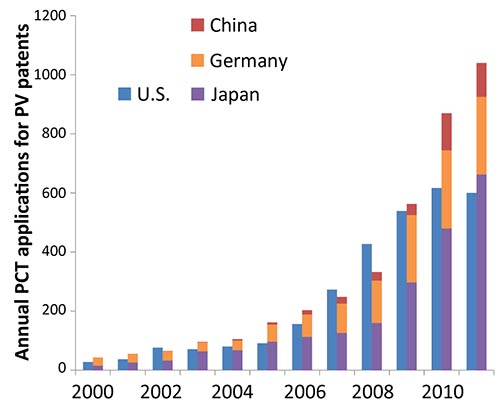

Fig. 3. PCT applications for PV-related patents by international filing date during 2000–2011. (Please refer to the paper for details.)

As shown in Fig. 3, what worries us most is that the innovation pace showed signs of slowing down in 2011, the latest patent data publicly available. As we are still counting on the cost of PV technologies to come further down, we need more innovation, not less.

What are the policy adjustments we need for a sustainable global PV industry?

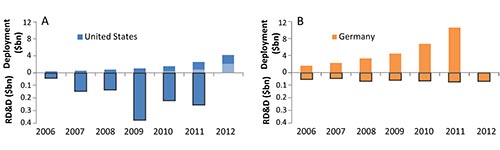

Fig. 4. Funding allocation between public R&D and deployment for solar PV. The cash grant (from the American Recovery and Reinvestment Act), as part of the deployment funding, is highlighted in lighter color. (Please refer to the paper for details.)

First, we need to adopt a more balanced budget between deployment incentives and public research and development (R&D) investment. As shown in Fig. 4, Germany’s public R&D budget in 2011, including funding for demonstration projects, was about $70 million US dollars, which was less than 1% of the $10.6 billion US dollars spent as feed-in tariff payment.

Second, energy policies towards solar PV should lean towards an innovation-focused roadmap and focus less on further market scale-up in this transitional phase. Using different models to analyze the historical deployment and price data of wafer-based PV modules and thin film PV modules, we reached the same conclusion: an innovation-focused roadmap is more effective in both meeting the cost target by 2020 and the required learning investment (or in other words the cost).

Third, the deployment incentives need some refinements to align with the strategic goal of channeling the financial resources towards more innovative and promising PV manufacturers.

Most importantly and in the immediate term, international coordination in deployment policies is needed to help end the oversupply problem sooner and offer a financially healthy environment for PV manufacturers to function and innovate again.

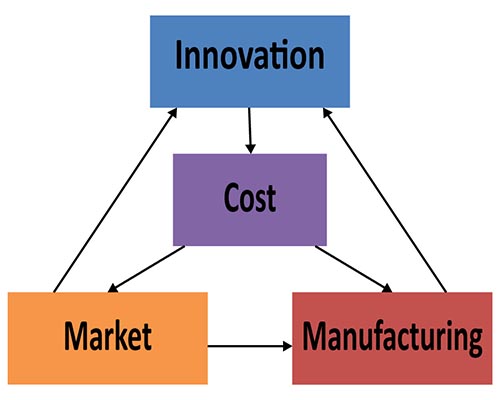

Fig. 5. The conceptual model for building an innovation-driven and sustainable PV industry. (Please refer to the paper for details.)

Putting these pieces together, policies on the national level could adopt a more holistic approach and utilize the reinforcing dynamics (Fig. 5) among market, manufacturing, innovation, and cost, to build a sustainable PV industry.

The corresponding author, Dr. Daniel Kammen, is the Class of 1935 Distinguished Professor of Energy at the University of California, Berkeley, with parallel appointments in the Energy and Resources Group, the Goldman School of Public Policy, and the department of Nuclear Engineering. He is also the founding director of the Renewable and Appropriate Energy Laboratory (RAEL), Co-Director of the Berkeley Institute of the Environment, and Director of the Transportation Sustainability Research Center.

Mr. Cheng Zheng is currently a PhD candidate in the Mechanical Engineering department at the the University of California, Berkeley. He is also the co-chair of the PV Idea Lab, a graduate student and postdoc platform to present, collaborate, and network on campus.

The paper: An innovation-focused roadmap for a sustainable global photovoltaic industry

Dr. Kammen's interview "Big solar and renewable energy in the age of fracking" on OnPoint with Tom Ashbrook (Feb 19, 2014)